Having a good time? Desire to do another? Enjoying the enthusiasm. For our 3rd example, let's turn to Melvin. He's 47 years old, remains in great but not excellent health, doesn't smoke and lives in the City by the Bay: San Francisco. He desires a 20-year policy with a protection quantity of $100,000, and he wants his premiums back at the end of the term.

His premiums are a bit greater than Jane's since he's older, and he desires the money-back warranty of a Return of Premium policy. On the other hand, they're lower than Dale's due to the fact that Melvin is in good health and does not smoke. Plus, he only desires coverage for the next 20 years, and for a much smaller amount than Dale.

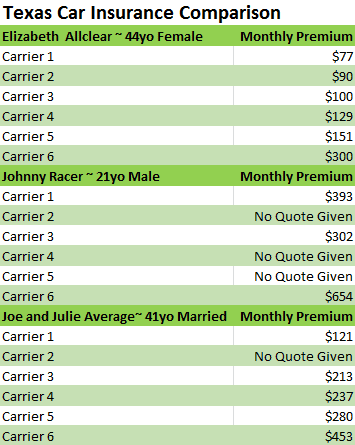

If you're thinking of purchasing life insurance, it is necessary to comprehend these elements, as well as the kinds of policies that might work for you. As soon as you have actually chosen a specific policy, it's time to compare life insurance quotes, and, lastly, partner with the business you're most comfortable with.

Purchase a 10-year term policy to supplement your existing life insurance. Possibly you prepared ahead when you were young and bought life insurance coverage right after your very first kid. You locked in a great low premium payment for a 30-year, $250,000 term policy. Perfect. But 15 years later on you're now 40 and realize that your $250,000 term life insurance coverage policy will not cover your $400,000 home loan.

How Long Do You Have To Have Life Insurance Before You Die Fundamentals Explained

This will ensure that you have a suitable amount of protection for the next 10 years while you're paying off your home mortgage and through your child( ren) through their college yearswithout being over-insured. Buy a 10-year term life insurance coverage policy to protect a loan. Whether you require to take out an individual or organization loan, lending institutions need to know how you intend on repaying the loan.

Lenders will be more inclined to authorize your loan if you designate a term life insurance policy to guarantee payment even upon death. Buy a 10-year term policy if you are close to retirement. The majority of the time term life insurance coverage policies are bought to cover the most economically vulnerable years, such as when your children are little, and you have quite a few years left on your mortgage.

For instance, let's say you are 55-years old and you and your partner finally purchase that dream condo on the ocean. It will be a terrific location for your kids and grandchildren to go to. Nevertheless, among your children hasn't finished college and tuition isn't low-cost. You have savings and your Social Security advantages will be starting quickly.

Retirement and your monetary future. Hmm. you'll navigate to considering it one day. And life insurance coverage? That too. However here's the funny feature of lifewe can't control it - what is universal life insurance. Things occur that we never ever see coming, and there's very little we can really prepare for. That's why it's so essential to get things in location right now that we can controllike life insurance.

When To Get Life Insurance Fundamentals Explained

When you boil things down, you actually have 2 alternatives when it comes to life insuranceterm vs. entire life. One is a safe strategy that assists safeguard your household and the other one, well, it's a total rip-off. Term life insurance supplies life insurance protection for a specific amount of time.

Term life insurance coverage strategies are much more budget-friendly than entire life insurance coverage. This is due to the fact that the term life policy has no money value until you or your partner dies. In the most basic of terms, it's not worth anything unless among you were to pass away during the course of the term.

Of course, the hope here is you'll never ever have to use your term life insurance coverage policy at allbut if something does take place, at least you understand your household will be taken care of. The premiums on entire life insurance (sometimes called money value insurance) are normally more pricey than term life for a number of reasons.

It may sound like an advantage to have life https://www.globenewswire.com/news-release/2020/06/10/2046392/0/en/WESLEY-FINANCIAL-GROUP-RESPONDS-TO-DIAMOND-RESORTS-LAWSUIT.html insurance protection for your whole life. However here's the fact: If you practice the concepts we teach, you will not need life insurance forever. Eventually, you'll be self-insured. Why? Since you'll have absolutely no financial obligation, a complete emergency fund and a substantial quantity of cash in your financial investments.

Fascination About How To Choose Life Insurance

It's like Dave states in his book The Total Guide to Cash, "Life insurance coverage has one job: It changes https://www.businesswire.com/news/home/20191125005568/en/Retired-Schoolteacher-3000-Freed-Timeshare-Debt-Wesley#.Xd0JqHAS1jd.linkedin your income when you die." There are far more efficient and rewarding methods to invest your cash than utilizing your life insurance plan. What seem like more enjoyable to youinvesting in growth stock shared funds so you can enjoy your retirement or "investing" cash in a plan that's all based on whether you bite the dust? We believe the answer is pretty easy.

He search and finds he can purchase an average of $125,000 in insurance for his household. From the entire life insurance representative, he'll most likely hear a pitch for a $100 per month policy that will construct up cost savings for retirement, which is what a money value policy is supposed to do.

So, if Greg goes with the whole life, cash value option, he'll pay a large regular monthly premium. And the part of his premium that isn't going towards in fact insuring him, goes towards his cash value "financial investment," right? Well you 'd believe, however then come the costs and expenses. That additional $82 monthly vanishes into commissions and expenditures for the first 3 years.

Worse yet, the savings he does manage to develop after being swindled for 20 years won't even go to his household when he passes away. Greg would have required to withdraw and invest that money worth while he was still alive. Speak about pressure! The only benefit his household will get is the stated value of the policy, which was $125,000 in our example.

The Ultimate Guide To How Much Life Insurance Do I Need

That's a great deal of bang for your dollar! You ought to buy a term life insurance coverage policy for 1012 times your annual earnings. That way, your income will be changed for your household if something occurs to you. You can run the numbers with our term life calculator. And do not forget to get term life insurance for both spouses, even if one of you stays at house with the kids.

Desire to ensure your household is covered no matter what occurs? Look at your protection before it becomes an emergency. Take our 5-minute coverage checkup to make certain you have what you https://www.inhersight.com/companies/best/reviews/salary?_n=112289587 require. Dave advises you purchase a policy with a term that will see you through up until your kids are avoiding to college and living on their own.

A great deal of life can take place in twenty years. Let's say you get term life insurance coverage when you're 30 years old. You and your spouse have an adorable little two-year-old young child running around. You're laser-focused on paying off all your financial obligation (consisting of your house) and look forward to investing and retirement preparation in the future.